- Advance Genie

- Posts

- The $1 Million Cutoff: What Financial Analysts Predict for 2026

The $1 Million Cutoff: What Financial Analysts Predict for 2026

Major forecasting firms agree on these three shifts

Welcome to Advance Genie, the newsletter that helps operators in high-friction industries find smarter paths to capital.

As 2025 closes, we analyzed over 75 prediction reports from Deloitte, McKinsey, BCG, EY, KPMG, and major financial research firms. We found an interesting consensus on several fronts, with notable disagreements on others.

Here's what the world's top financial analysts predict for 2026..

📬 Enjoying Advance Genie?

We're a small newsletter trying to reach/help founders and operators in high-friction industries.

If you find this useful, please forward this edition to someone who might benefit - a fellow founder, a friend, colleague, or anyone interested in these topics.

Thank you for helping us. 🙏

Three Channels Replacing Bank Lending

Basel III Endgame capital requirements have made loans under $1 million mathematically unprofitable for traditional banks. The regulatory burden of originating, servicing, and holding a $500,000 business loan now exceeds the net interest income banks can generate from it.

Small Business Currents, citing executives from Biz2Credit, Cardiff, and major fintech lenders, makes the most consequential prediction for 2026: by Q4 2026, private fintech lenders will surpass regional banks as the primary source of growth capital for American small businesses.

William Stern, founder of Cardiff, framed it bluntly: "This isn't a cycle. It's a structural exit."

Grand View Research projects the alternative lending platform market will grow from $3.82 billion in 2024 to $14.47 billion by 2030, a compound annual growth rate of 25.4%.

That's four times faster than the overall banking sector.

Embedded Finance Reaches Scale

The data shows significant SMB adoption intent: 50% of small and medium businesses express high likelihood of utilizing the full suite of embedded finance products in the near future.

BCG projects B2B platform transaction volumes will exceed $7 trillion by 2026 in the United States alone.

SaaS platforms embedding financial products can amplify revenues 3-4x compared to subscription fees alone.

The mechanics are straightforward: a restaurant using Toast for point-of-sale accesses capital directly within the dashboard, underwritten instantly using transaction history. A construction contractor using Procore for project management gets banking, payments, and equipment financing as integrated features.

The software becomes the financial services provider.

SaaS providers with integrated payments are projected to capture 45% of SME acquiring revenues by 2028.

AI Decisioning Goes Operational

Multiple sources including EY, McKinsey, and VoPay predict that by 2026, over 70% of financial institutions will deploy AI decisioning tools under strict governance frameworks.

Forrester goes further: approximately 1/3 of B2B payment workflows will use autonomous AI agents by year-end 2026.

Traditional bank underwriting submits tax returns, personal financial statements, and business plans. A human reviews documents and runs credit checks over 30-60 days.

The decision is based primarily on credit score and collateral.

AI-powered embedded finance underwriting grants API access to banking and commerce accounts. AI analyzes six months of transaction data, identifies revenue patterns, calculates cash flow volatility, and assesses seasonal trends.

Decision in under four minutes. Funding same day.

QED Investors calls this the rise of "dynamic credit scoring" using alternative data streams: banking data, rent payments, utility payments, supplier payment history, and real-time transaction flows.

Approval workflows will shrink from days to minutes via API integrations.

Revenue-Based Financing Matures

Multiple sources predict revenue-based financing will see double-digit growth in 2026, but the model has evolved significantly from its earlier iteration.

The 2026 RBF model is characterized by:

Specific use cases: inventory restock, advertising spend spikes, equipment purchases

Shorter durations: 3-9 months rather than multi-year facilities

100% automated underwriting via API connections to banking and commerce data

Offered by both specialized fintechs and vertical SaaS platforms as white-labeled products

Repayments scale automatically with revenue. If sales slow, payments adjust down. If business accelerates, payback happens faster.

This automatic adjustment goes in line with working capital needs for businesses facing regulatory uncertainty and fluctuations.

The Stablecoin Disagreement

The most contentious prediction for 2026 involves stablecoins.

Major financial firms agree on institutional adoption and regulatory clarity, but disagree sharply on retail consumer adoption timelines.

The Bull Case: Overtaking ACH

Galaxy Digital's research team makes the boldest prediction: stablecoins will overtake ACH transaction volume in 2026.

The data supporting this view:

Stablecoins processed $9 trillion in payments in 2025, an 87% jump from 2024

Analysis shows stablecoins currently process approximately 50% of ACH volume

Stablecoin transaction volume already exceeds Visa ($15.7 trillion) and Mastercard ($9.8 trillion) in annual payment processing

Stablecoin market cap - $309 billion with 30-40% supply growth CAGR

Visa's corporate predictions state: "2026 is the year stablecoins truly take off. The potential for stablecoins to add to and complement the existing global payment ecosystem is enormous, especially for emerging markets and for cross-border."

The Bear Case: B2C Won't Happen

Forrester Research offers a different view. Analyst Lily Varon predicts stablecoins will NOT become mainstream for retail consumer payments in 2026.

The supporting evidence:

Only 24% of US online adults trust AI to make routine purchases on their behalf

Consumer payment habits change slowly

Stablecoins will remain niche in B2B cross-border and crypto-native economy

4 out of 5 local stablecoin launches in Asia-Pacific will fail

Varon notes: "It's still such early days. Many agentic commerce announcements aren't really product launches, they're just partnership announcements."

Where They Agree: B2B Infrastructure

Despite the retail disagreement, consensus exists on business-to-business infrastructure adoption.

The GENIUS Act, signed into law in July 2025, established the first federal framework for payment stablecoins in the United States. Regulations become effective January 2027, but institutions are integrating now.

Deloitte's December 2025 payments report finds that nearly half of financial institutions already use stablecoins, with 41% planning adoption in the near term.

Visa's monthly stablecoin settlement volume exceeded $3.5 billion annualized run rate as of November 2025. Visa currently supports 130+ stablecoin-linked card programs in 40+ countries.

Major banks are launching their own stablecoins: JPMorgan is extending JPM Coin beyond institutional clients. A consortium of US banks including PNC, Citi, and Wells Fargo is exploring a joint stablecoin through Early Warning Services, the company that operates Zelle.

The consensus view: B2B cross-border payments will see explosive stablecoin adoption in 2026, while retail consumer adoption remains years away.

Three Specific Predictions Worth Tracking

McKinsey's $170 Billion Profit Pool Wipeout

McKinsey's Global Banking Annual Review introduces a critical framework for 2026: "Precision vs. Heft."

The Era of Heft (2010-2024): Banks won by being big. They acquired millions of users, often unprofitably, rolled out generic digital apps, and relied on rising interest rates to generate net interest income regardless of operational efficiency.

The Era of Precision (2026+): Size is no longer a protective moat. In a world of agentic AI and open finance, customers can switch providers instantly. Winners use precision by using proprietary data to offer the exact right product at the exact right moment.

McKinsey predicts that banks sticking to the "Heft" model could lose $170 billion in profit pools by 2030 to specialized agents and platforms.

This trend favors vertical fintechs, a bank specifically for construction firms, over horizontal neobanks offering generic checking accounts. Precision beats scale in a saturated market.

The Speed vs Cost Trade-Off Inverts

William Stern, founder of Cardiff, predicts a fundamental shift: "The real barrier for small businesses right now isn't the price of money, it's the speed of it. Even a 'cheap' bank loan is useless if it takes 45-60 days to approve."

The current market segmentation:

Bank loans: 7-12% APR, 30-60 day approval timeline

Fintech loans: 15-35% APR, same-day funding

For businesses needing working capital to capture an immediate opportunity or cover an urgent gap, the 45-day wait makes the cheaper option worthless.

By Q4 2026, multiple sources predict speed will become the primary competitive advantage over cost for small business lending.

The 70% AI Adoption Threshold

EY, McKinsey, and VoPay all land on the same figure: over 70% of financial institutions will deploy AI decisioning tools by 2026.

This isn't a pilot program. These are production deployments under strict governance frameworks.

American Banker's survey of 174 banking professionals (October-November 2025) found 20% cite AI advancements as their top prediction for 2026, the highest-ranking category.

One survey respondent: "AI will have a bigger impact than expected. It already has but it will be exponential through 2026."

The implementation details from EY's regulatory outlook:

16% have fully deployed AI solutions,

52% are running pilot projects,

institutions expect 20-30% year-over-year increases in compliance workload for AML, fraud monitoring, and data privacy.

The governance challenge is quite big with regulators demanding "kill switches" and rigorous monitoring for autonomous AI systems.

The "black box" problem is a major legal liability.

Banks must be able to explain why an AI denied a loan or flagged a transaction so explainable AI becomes a mandatory requirement for any deployed model in 2026.

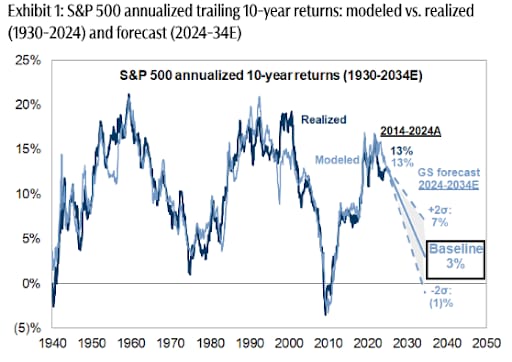

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

What'd you think of this issue? |